The Survival Threshold of Pay-at-Harvest Insurance: Strategic Default and Institutional Enforcement

Abstract:

Pay-at-harvest agricultural insurance has been proposed as a promising mechanism for expanding risk protection among liquidity-constrained smallholder farmers by postponing premium payments until harvest. However, the long-term viability of pay-at-harvest insurance under unconstrained market conditions remains insufficiently understood. Using experimental evidence from Kenya, an unconstrained endogenous default rate of 54.11% was identified, with default behavior being primarily driven by rational intertemporal arbitrage rather than by ex-ante adverse selection. To evaluate the implications of this behavioral friction for market sustainability, the observed default behavior was incorporated into an infinite-horizon dynamic game and a state-dependent actuarial framework. The analysis demonstrates that absorption of the baseline default rate would require an actuarially fair premium surcharge of approximately 85.16%, thereby generating severe adverse selection pressures. A closed-form survival threshold was subsequently derived, revealing that actuarial sustainability can be maintained only when the endogenous default rate is suppressed below 5.60%. To identify mechanisms capable of achieving this threshold, an ex-ante institutional design framework was calibrated using features commonly observed in rural China’s agricultural market architecture. It is shown that overlapping closed-loop enforcement mechanisms—including contract-farming relationships, financial cross-default arrangements, and algorithmic credit monitoring systems—can operate as intertemporal commitment devices that substantially increase the shadow cost of strategic default. Under plausible parameterizations, these institutional arrangements are predicted to compress the equilibrium default rate to approximately 5.00%, thereby satisfying the actuarial survival condition. The results indicate that financial innovation in agricultural risk management must be accompanied by commensurate enforcement capacity if durable and scalable insurance markets are to be achieved.1. Introduction

Agricultural insurance is universally recognized as a critical tool for mitigating production risks and smoothing consumption among smallholder farmers in developing countries. However, voluntary take-up of standard indemnity or index-based insurance remains persistently low (Cole et al., 2013). A central explanation in the recent development economics literature is the presence of severe intertemporal liquidity constraints: standard insurance strictly requires upfront premium payments at planting, precisely when farmers’ liquidity is most exhausted by input purchases (Giné & Yang, 2009; Karlan et al., 2014). To resolve this intertemporal friction, the pay-at-harvest mechanism has emerged as a profound financial innovation. By deferring the premium payment until the realization of harvest revenues, pay-at-harvest functions as a bundled product of risk protection and a short-term liquidity loan. Seminal experimental evidence, notably by Casaburi & Willis (2018) in Kenya, demonstrates that shifting from upfront payments to pay-at-harvest can dramatically increase insurance demand from 5% to 72%. However, the prevailing literature exhibits a pronounced demand-side bias. An often-overlooked boundary condition of early pay-at-harvest successes is their implementation within strictly controlled contract farming environments, where agribusiness buyers can directly deduct premiums from harvest revenues, perfectly enforcing repayment.

This study ask

s a fundamental supply-side question: What happens to the actuarial sustainability of pay-at-harvest mechanisms when such stringent enforcement constraints are relaxed in an open, decentralized market? When farmers possess the strategic option to default on deferred premiums—particularly in states of the world where yields are moderate but no insurance payout is triggered—the insurer is inadvertently transformed into an uncollateralized lender, exposed to severe endogenous moral hazard. This study bridges the gap between demand-driven enthusiasm and supply-side actuarial reality by making three primary contributions. First, utilizing randomized controlled trial data from the Kenyan agricultural market—serving as a proxy for an unconstrained, decentralized spot market—a baseline endogenous default rate of 54.11% is identified. Controlling for selection on observables and conducting heterogeneity analysis, the result demonstrates that this high default rate is not merely an artifact of initial adverse selection, but a rational economic response driven by intertemporal liquidity preferences.

Second, this study embeds this empirical baseline into a state-dependent actuarial pricing framework. The result demonstrates that in a static setting, the incentive compatibility constraint structurally fails. To absorb a 54.11% default rate, insurers must impose a prohibitive premium surcharge of 85.16%, which inevitably triggers an adverse selection death spiral. By modeling the farmer’s decision as an infinite-horizon repeated game, this study mathematically derives a strict “survival threshold”. The research proves that for a pay-at-harvest market to be commercially viable without perpetual external subsidies, the maximum tolerable endogenous default rate must be rigorously capped at ≤5.60%. Third, this study conducts an ex-ante mechanism design calibration situated within the institutional landscape of rural China, evaluating how macro-level infrastructure can satisfy this micro-level 5.60% threshold. This study formalizes three “closed-loop” enforcement mechanisms—physical closed loops (contract farming monopsonies), financial cross-defaults (rural credit cooperatives), and digital panopticons (mobile payment credit scoring). The dynamic sensitivity analysis in this study proves that these overlapping mechanisms effectively increase the intertemporal penalty of default, driving the default rate down to approximately 5.00% and transitioning the market into a Pareto-improving equilibrium.

Ultimately, this study argues that financial innovation cannot precede institutional capacity. The successful deployment of liquidity-enhancing mechanisms like pay-at-harvest is strictly conditional on an economic architecture capable of enforcing micro-contracts over time. As structurally outlined in Figure 1, readers should interpret this roadmap as a progression from documenting a market failure (Stages 1 & 2) to engineering an institutional solution (Stage 3).

2. Institutional Background and Literature

This research sits at the intersection of three distinct strands of literature: the alleviation of liquidity constraints in agriculture, the microeconomics of uncollateralized credit and relational contracts, and the rise of digital financial ecosystems.

The fundamental failure of agricultural insurance markets in developing economies is typically analyzed through the lenses of basis risk (Clarke, 2016), compound-risk aversion (Elabed & Carter, 2015), or liquidity constraints. Deferring premium payments directly targets the liquidity friction. Casaburi & Willis (2018) provide the most robust experimental benchmark, proving that pay-at-harvest acts simultaneously as a risk-mitigation tool and intra-seasonal credit provision. Similar mechanisms have been explored to boost technology adoption and input usage (Casaburi & Macchiavello, 2019). However, this literature primarily isolates the demand-side treatment effect. This study pivots to the supply side, formally quantifying the actuarial boundaries required to sustain this liquidity provision at scale (Carter et al., 2017).

By deferring premiums, insurers essentially issue uncollateralized micro-loans. In traditional agricultural credit markets, asymmetric information and the absence of collateral lead to credit rationing, moral hazard, and strategic default (Stiglitz & Weiss, 1981). When pay-at-harvest is introduced outside tightly controlled environments, it inherits these exact informational frictions. To resolve this, the literature points to relational contracts and supply chain integration. As demonstrated by Macchiavello & Morjaria (2021) in the Rwandan coffee chain and Swinnen & Maertens (2007) in broader developing contexts, vertical coordination and the promise of future rents can enforce current-period compliance. This study builds upon this foundation by modeling the pay-at-harvest default decision as an infinite-horizon repeated game, where the institutional penalty is the discounted loss of future contract farming rents (Bellemare, 2012). This provides the theoretical micro-foundation for the proposed physical “closed-loop” mechanism.

Finally, this study contrasts the unconstrained empirical baseline with the institutional evolution of rural China to identify practical solutions. The rise of digital finance has profoundly altered the transaction costs of enforcement and relaxed historical capital barriers. Recent macro-level evidence confirms that digital financial inclusion significantly alleviates farmers’ credit constraints, thereby driving agricultural modernization and the adoption of mechanization services in China (Yan et al., 2025). Building upon this macro-level transformation, micro-level literature on alternative credit scoring demonstrates that behavioral data and mobile phone usage can effectively predict and constrain repayment behavior (Björkegren & Grissen, 2020).

However, the unconstrained introduction of digital finance and insurance tools is not a panacea. Recent emerging evidence highlights an “agribusiness paradox” where introducing insurance in low-marketization regions without sufficient institutional enforcement can trigger a transparency trap and inadvertently exacerbate credit constraints (Chong & Wang, 2026). This paradox directly underscores the core thesis of this study: the viability of pay-at-harvest insurance requires more than mere financial digitalization. In China, the pervasive integration of mobile payment systems (e.g., WeChat Pay and Alipay) and rural credit cooperatives essentially merges a farmer’s social, commercial, and financial identities. By conceptualizing these digital and financial networks as overlapping “closed loops”, the proposed framework moves beyond localized randomized controlled trials to evaluate how macro-level digital infrastructure alters the micro-incentives of strategic default, thereby rendering pay-at-harvest insurance actuarially sound.

3. Empirical Baseline and Parameter Identification

To rigorously evaluate the supply-side sustainability of the pay-at-harvest mechanism, this study first establishes an empirical baseline that isolates farmers’ default behavior in an unconstrained environment. Randomized controlled trial data from Kenyan sugarcane farmers is utilized, which serves as an ideal proxy for a decentralized, fragmented spot market lacking coercive debt enforcement mechanisms.

To empirically ground the proposed structural model, this study utilizes micro-level survey and administrative data from a randomized controlled trial involving smallholder sugarcane farmers in Kenya. The agricultural landscape in this region provides an ideal testing ground for unconstrained pay-at-harvest dynamics. While initial pay-at-harvest experiments were tightly embedded within monopolistic contract farming schemes, a significant portion of the sample in this study operates with access to decentralized spot markets (side-selling avenues) and possesses heterogeneous institutional trust, allowing us to observe the baseline friction of strategic default. The full dataset comprises N = 324 farmers. Demographic and agronomic baseline characteristics indicate a representative smallholder population. The average farmer in the sample is approximately 45 years old, cultivating a relatively small plot with a mean land size of 1.4 acres. This land constraint exacerbates vulnerability to yield shocks and intertemporal liquidity crunches. Baseline financial inclusion is notably weak; when assessing initial wealth and liquidity buffers, a substantial proportion of farmers reported lacking sufficient baseline savings to cover standard pre-harvest input costs (e.g., fertilizers and upfront insurance premiums).

Before examining the supply-side frictions, whether the sample of this study validates the demand-side hypotheses established in the pay-at-harvest literature must be verified. This study estimates a linear probability model to formalize the demand equation, presented in Table 1. Consistent with prior findings, the introduction of the pay-at-harvest mechanism fundamentally transforms the uptake decision by eliminating the intertemporal transfer friction. The treatment assignment to the pay-at-harvest scheme increases the absolute probability of purchasing insurance by 71.5 percentage points (p < 0.01). Furthermore, the data of this study allows us to control for selection on observables. Baseline savings exhibit a significant negative correlation with insurance demand (coefficient -0.075, p < 0.05). This indicates that farmers with severe liquidity constraints are the primary beneficiaries of the deferred premium model. Conversely, the “trust index”—a composite metric capturing the farmer’s self-reported trust in both the insurance company’s field assistants and regional managers—remains a positive and significant covariate (coefficient 0.033, p < 0.05). This highlights that while pay-at-harvest solves the liquidity problem, baseline institutional trust remains a prerequisite for initial contract formation.

Independent Variables | (1) | (2) | (3) |

Baseline | With Controls | Heterogeneity | |

Treatment (Pay-at-harvest) | 0.732∗∗∗ (0.048) | 0.715∗∗∗ (0.045) | 0.680∗∗∗ (0.052) |

Log (baseline savings) | -0.075∗∗ (0.032) | -0.081∗∗ (0.034) | |

Trust index (0–10) | 0.033∗∗ (0.015) | 0.029∗ (0.016) | |

Plot size (Acres) | 0.012 (0.018) | 0.015 (0.019) | |

Age | 0.004 (0.003) | 0.003 (0.003) | |

Pay-at-harvest × log (Savings) | 0.042∗ (0.021) | ||

Constant | 0.051∗∗ (0.021) | 0.284∗∗ (0.112) | 0.276∗∗ (0.115) |

Village fixed effects | No | Yes | Yes |

Observations | 324 | 324 | 324 |

R2 | 0.421 | 0.485 | 0.492 |

Crucially, even after controlling for these observables and incorporating village-level fixed effects, the magnitude of the pay-at-harvest treatment effect remains stable. This confirms that the sample of this study accurately represents a population highly responsive to liquidity provision, effectively ruling out systemic sample selection bias and setting a valid, robust stage for the subsequent supply-side stress test.

The critical parameter for the proposed actuarial model is the strategic default rate when farmers do not experience systemic weather shocks. Within the core pay-at-harvest intervention group (N = 146), the empirical compliance rate—measured by farmers delivering their harvest to the designated agribusiness—is merely 45.89%. Consequently, the pure endogenous default (side-selling) rate, denoted as πno_shock, is precisely identified at 54.11%.

To ensure that this 54.11% default rate represents a genuine institutional friction rather than a mere artifact of adverse selection, this study conducts robustness checks based on selection on observables. The baseline default rate remains highly robust after controlling for covariates such as age, baseline savings, and land size. Furthermore, this study explores the heterogeneity of default behavior across different farmer sub-groups. As illustrated in Figure 2, farmers with larger landholdings or higher initial savings exhibit a marginally decreasing propensity to default.

To further rule out the concern that the baseline rate is driven by localized spatial correlation or village-level collusion, this study examines geographic heterogeneity. Figure 3 plots the village-level aggregates, demonstrating a robust negative correlation between aggregated institutional trust and the endogenous default rate across different geographic clusters. This confirms that the high default rate is a systemic intertemporal friction rather than a localized anomaly. This baseline parameter (πno_shock = 0.5411) forms the empirical foundation for the proposed structural pricing model.

4. Micro-Foundations of Default and the Dynamic Contract Model

This study now bridges the empirically observed 54.11% default rate with a micro-founded structural model. This section constructs an intertemporal incentive compatibility constraint to quantify behavioral frictions, subsequently embedding them into a state-dependent actuarial pricing framework.

In a given crop cycle, let pshock denote the probability of a systemic weather shock, and 1 − pshock the probability of a non-shock state. In the shock state, the insurer deducts the premium directly from the indemnity payout, structurally enforcing compliance ($\pi_{\text {shock }}^*$ = 0). However, in the non-shock state, the farmer faces a strategic choice: comply and pay the premium Pbe, or default by side-selling the harvest to a spot market at a price wedge ∆ ≥ 0. Let $C_{\text {inst }}$ denote the institutional penalty for default. Assuming risk neutrality for marginal deviations in cash flow, a rational farmer will comply in a single-period static setting if and only if:

In the Kenyan baseline context, the absence of coercive enforcement drives the institutional penalty toward zero ($C_{\text {inst }}$ → 0). Because the premium is strictly positive, the static incentive compatibility constraint is structurally violated. This micro-level failure serves as the root cause for the macro-level 54.11% endogenous default rate.

To transcend the limitations of a static perspective, this study models the farmer’s decision as an intertemporal dynamic game without a deterministic end date. In this framework, a farmer’s default is not merely a one-time cash flow arbitrage, but a severance of relational contracts with the supply chain or credit system. Introducing a discount factor $\delta \in$ (0,1), if a farmer defaults, the short-term payoff is the evaded premium and the spot market wedge (Pbe + ∆). However, the long-term cost is permanent exclusion from the closed-loop system, forfeiting the discounted present value of all expected future supply chain rents or credit access, denoted as $\sum_{t=1}^{\infty} \delta^t E\left[\Pi_{\text {future }}\right]$. Thus, the dynamic incentive compatibility constraint is reconstructed as:

This model profoundly reveals the survival logic of the pay-at-harvest mechanism: endogenous default can only be effectively suppressed if farmers exhibit sufficient patience (a sufficiently large δ) or if the closed-loop mechanism provides substantial expected future rents ($E\left[\Pi_{\text {future }}\right]$). Figure 4 visually distills this intertemporal trade-off. The critical takeaway from this decision tree is that pay-at-harvest sustainability relies entirely on inflating the bottom-right node (long-term institutional penalty) to outweigh the bottom-left node.

This study embeds this dynamic default behavior into an actuarial model. Let the frictionless base premium be $P_{\text {base }}=p_{\text {shock }} \times L+C_{\text {admin }}$. Using standard empirical parameters (policy limit L = 400 RMB, shock probability pshock = 0.15, administrative cost Cadmin = 15 RMB), the base premium Pbase is = 75 RMB. Since defaulting farmers in the non-shock state cannot be coerced to pay, the expected effective collection rate (E[CR]) is:

Substituting the empirical 54.11% default rate, E[CR] plummets to 54.01%. To maintain actuarial balance, the insurer must impose a risk premium, driving the break-even premium to Pbe = 138.87 RMB. The implied risk loading (λ) is therefore:

An 85.16% risk loading acts as an expropriative tax on low-risk compliant farmers. This severely violates the individual rationality constraint, triggering a classic adverse selection death spiral. The causal loop in Figure 5 demonstrates the precise operational collapse mechanism: the 85.16% expropriative tax forces low-risk farmers out, which mathematically ensures the subsequent cycle will face an even higher endogenous default rate.

To rigorously ground the actuarial pricing simulation in realistic market conditions rather than arbitrary assumptions, the parameters introduced in the proposed state-dependent model are explicitly anchored to official agricultural insurance guidelines and empirical climatic risks. Table 2 summarizes the parameter definitions, their baseline values, and the real-world selection criteria based on China’s policy-based agricultural insurance framework.

Parameter | Definition | Baseline Value | Source & Selection Criteria |

L | Policy limit (Sum insured) | 400 RMB | Typical basic sum insured per mu for staple crops covering direct material costs (Ministry of Finance of the People’s Republic of China, 2022). |

pshock | Systemic shock prob. | 0.15 | Standard “1-in-7 year” severe weather event. |

Cadmin | Administrative cost | 15 RMB | Calibrated to exactly a 20% expense ratio, aligning with the Ministry of Finance regulatory cap (Ministry of Finance of the People’s Republic of China, 2024). |

$\bar{\lambda}$ | Max tolerable loading | 5% | Anchored to the “break-even and low-profit” regulatory principle for agricultural insurance. |

To sustain the market and prevent adverse selection, this study establishes a commercially tolerable upper bound for the risk loading at This restricts the break-even premium to Pbe ≤ 78.75 RMB. By substituting this condition back into the collection rate equation, it can be found that E[CR] must satisfy E[CR] ≥ 95.24%. Solving for the endogenous default rate yields the theoretical red line:

This stringent survival threshold (5.60%) mathematically proves that for the pay-at-harvest mechanism to survive independently without external subsidies, it must be embedded within a robust institutional environment capable of compressing moral hazard by an order of magnitude relative to the unconstrained baseline.

5. Institutional Constraints and Market Viability: The Closed-Loop Calibration

Before detailing the mechanism calibration, it is necessary to clarify the rationale for transitioning from the Kenyan empirical setting to the Chinese institutional context. In this framework, the randomized controlled trial data from Kenya functions exclusively as the unconstrained natural baseline—it isolates the pure behavioral friction of strategic default in a decentralized spot market lacking coercive debt enforcement. However, testing the theoretical boundaries of the survival threshold (the mathematically required ≤5.60% default rate) necessitates observing an advanced enforcement architecture. Rural China provides an ideal institutional target environment. Unlike the fragmented unconstrained baseline, China’s recent agricultural modernization has produced deeply integrated physical, financial, and digital infrastructures. Transitioning to this setting allows us to formally calibrate how macro-level closed-loop systems function as exogenous constraints to alter micro-level intertemporal default behaviors, thereby demonstrating the mechanism’s cross-institutional applicability.

Having established that a sustainable pay-at-harvest market in a frictionless environment strictly requires an endogenous default rate of ≤5.60%, this study now pivots to an ex-ante institutional analysis. This research argues that the unconstrained Kenyan baseline (54.11%) is not an inherent flaw of pay-at-harvest, but rather a symptom of institutional voids. To satisfy the survival threshold, the dynamic institutional penalty for default must structurally outweigh the short-term spot market arbitrage.

In the context of China’s rural revitalization and agricultural modernization, a highly integrated market architecture has emerged. This architecture can be conceptualized as a series of “closed-loop” enforcement mechanisms. Recalling the dynamic incentive compatibility constraint from Section 4, the institutional penalty Cinst is functionally equivalent to the discounted present value of future supply chain and credit rents.

China’s closed-loop institutional arrangements generate a high E[Пfuture] across three intersecting domains:

Physical Closed-Loops (Monopsonistic Supply Chains): The deep penetration of the “company + farmer” model establishes localized agribusiness monopsonies. Defaulting on a single pay-at-harvest premium equates to permanent exclusion from future high-yield seed provision and guaranteed purchase contracts. This aligns with comparative evidence across multiple developing nations, demonstrating that the threat of losing contract farming relationships serves as a universally binding constraint against micro-level defaults (Barrett et al., 2012).

Financial Closed-Loops (Cross-Default Linkages): Rural credit cooperatives increasingly bundle micro-insurance with spring-planting loans. A strategic default on the harvest-time insurance premium automatically triggers a cross-default clause on the farmer’s broader credit line, severing intertemporal liquidity access. This explicitly operationalizes the theoretical solution of interlinked contracts, demonstrating how tying credit directly with insurance effectively overcomes supply-side market failures (Carter et al., 2016).

Digital Closed-Loops (the Algorithmic Panopticon): Driven by a mobile payment penetration rate exceeding 88%, rural financial identities are inextricably linked to platforms like WeChat Pay and Alipay. Defaulting on a localized digital agricultural contract directly downgrades the farmer’s universal algorithmic credit score, imposing severe shadow costs on future consumption smoothing.

Figure 6 provides a macro-level mapping of these overlapping infrastructures. Rather than viewing them as isolated systems, the diagram illustrates how traditional village governance, commercial contracts, and digital algorithms collectively form an impenetrable boundary against default. Even in the absence of formal legal enforcement, these overlapping structures mirror the efficacy of informal reputation mechanisms and group constraints in ensuring micro-contract compliance (Dercon et al., 2014). When the pay-at-harvest mechanism is embedded within this overlapping tri-layered framework, the dynamic incentive compatibility constraint is fundamentally restructured. The combined threat of supply chain exclusion, credit termination, and digital algorithmic penalties ensures the following for the vast majority of farmers:

Through this institutional calibration, theoretical projections and localized pilot data indicate that the endogenous default rate (πno_shock) is systematically suppressed to approximately 5.00%. Because 5.00% is strictly less than the actuarial survival threshold of 5.60%, the pay-at-harvest market transitions from a state of adverse selection collapse to a Pareto-improving equilibrium, preserving the critical liquidity benefits for smallholder farmers.

The most novel, expansive, and uniquely Chinese constraint is the “digital closed-loop”. Unlike physical supply chains, which are crop-specific and geographically bound, the digital ecosystem permeates almost every node of a farmer’s economic life. Driven by a mobile payment penetration rate exceeding 88% globally—with deep rural integration predominantly through Tencent’s WeChat Pay and Ant Group’s Alipay—financial identities in rural China have become inextricably linked to social and commercial identities. As mobile payment systems fundamentally reshape consumption smoothing mechanisms, the shadow cost of digital exclusion becomes punitively high (Suri & Jack, 2016). Historically, the fundamental cause of credit rationing in rural markets was the absence of physical collateral and the prohibitively high cost of screening (Stiglitz & Weiss, 1981). However, platforms like MYbank (affiliated with Ant Group) have pioneered the use of “alternative data” as digital collateral. Every transaction, utility payment, agricultural subsidy receipt, and even social network interaction generates behavioral data. This data is aggregated into a universal, algorithmic credit scoring system (e.g., Sesame Credit). As demonstrated by recent multi-source data fusion models, these aggregated digital footprints have fundamentally evolved into “institutional hard constraints” for agricultural credit risk (Zhang et al., 2022).

When a pay-at-harvest micro-insurance contract is initiated via these digital platforms, it operates as an algorithmic smart contract. Defaulting on a localized harvest-time premium is no longer an isolated incident of side-selling; it instantly triggers an automatic downgrade of the farmer’s universal digital credit score. The penalty , therefore, represents the profound shadow cost of digital exclusion. A degraded score restricts the farmer from accessing zero-collateral micro-loans (“3-1-0” lending models: 3 minutes to apply, 1 second to approve, and 0 human intervention), disqualifies them from purchasing agricultural inputs on margin via e-commerce platforms (like Taobao), and disrupts daily consumption smoothing.

To illustrate this operational pathway of the “3-1-0” micro-credit concretely, consider a hypothetical smallholder farmer who attempts to strategically default on a 75 RMB pay-at-harvest premium after a normal harvest. Through the digital closed-loop (e.g., the Alipay ecosystem), this micro-default is instantly captured as alternative data, triggering an automated downgrade in their universal algorithmic credit score (such as Sesame Credit). When the next planting season arrives, the farmer faces a liquidity shortage for purchasing seeds and fertilizers. They attempt to apply for a zero-collateral spring planting loan through a digital lender like MYbank (which operates on a “3-1-0” model: 3 minutes to apply, 1 second to approve, and 0 human intervention). The smart contract queries the downgraded credit score and, recognizing the prior pay-at-harvest default, automatically rejects the loan application or significantly elevates the interest rate. The operational reality is that the shadow cost of losing access to vital intertemporal liquidity exponentially exceeds the 75 RMB arbitrarily saved during the previous harvest, practically eliminating the economic incentive to default.

Because the lifetime discounted utility of remaining within this digital ecosystem,

exponentially outweighs the marginal gain of evading a single insurance premium (Pbe), the incentive to default is systemically eradicated. Figure 7 shows the data flow and shadow costs of the algorithmic panopticon.

While the 5.60% threshold was derived under baseline parameters (pshock = 0.15, $\bar{\lambda}$ = 5%), macro-level agricultural environments are inherently heterogeneous. To evaluate the external validity of the proposed mechanism design, this study conducts a sensitivity analysis of the survival threshold. By generalizing the break-even constraint $E[C R] \geq \frac{1}{1+\bar{\lambda}}$, we derive a closed-form solution for the maximum tolerable endogenous default rate ($\pi_{\text {no_shock }}^*$):

This equation mathematically demonstrates that the survival threshold is an increasing function of both the market’s tolerance for premium surcharges ($\bar{\lambda}$) and the probability of systemic shocks (pshock). Figure 8 provides a contour heatmap illustrating the non-linear expansion of these survival zones. Complementing this visual analysis, Table 3 reports the precise maximum tolerable default rates under various bounds of commercial tolerance and baseline climatic risks.

Systemic Shock Probability (pshock) | Threshold at = 5% | Threshold at = 10% | Threshold at = 15% |

Low risk (pshock = 10%) | 5.29% | 10.10% | 14.49% |

Baseline (pshock = 15%) | 5.60% | 10.70% | 15.35% |

High risk (pshock = 20%) | 5.95% | 11.36% | 16.30% |

Table 3 reveals a profound policy insight: even under highly relaxed commercial tolerance ($\bar{\lambda}$ = 15%) and severe weather environments (pshock = 20%), the absolute ceiling for market survival is 16.30%. This remains radically lower than the unconstrained 54.11% baseline observed in the empirical data of this study.

The threshold variations in the sensitivity matrix presented in Table 3 carry specific operational and policy implications for agricultural environments. First, in high-risk environments where systemic shocks are frequent (e.g., pshock = 20%), the insurer’s fundamental margin is already heavily compressed by pure risk. Consequently, the system’s capacity to absorb behavioral friction shrinks, demanding an extremely rigorous institutional environment capable of suppressing the default rate closer to 5%. In practice, launching pay-at-harvest products in such regions necessitates the prior establishment of stringent supply-chain or digital enforcement. Second, the commercial tolerance parameter ($\bar{\lambda}$) dictates the division of cost-bearing. While a higher tolerance (e.g., $\bar{\lambda}$ = 15%) mathematically permits a higher default threshold (up to 16.30%), an open market cannot sustain such punitive risk loadings without triggering adverse selection. Therefore, operating in the upper bounds of this matrix implies a mandatory shift from market-driven premiums to heavy government subsidies. Ultimately, the sensitivity analysis highlights a trade-off: mitigating the strict institutional prerequisites for pay-at-harvest requires disproportionate public financial intervention to absorb the resulting moral hazard. Consequently, regardless of minor parameter fluctuations, the core conclusion remains robust: the deployment of pay-at-harvest mechanisms is strictly conditional on the macro-infrastructure’s capacity to enforce micro-contracts.

6. Conclusion

The pay-at-harvest mechanism represents a profound innovation in agricultural insurance, directly addressing the intertemporal liquidity constraints that have historically stifled demand in developing economies. However, this study demonstrates that the demand-side triumph of pay-at-harvest masks a critical supply-side vulnerability. By transforming insurers into uncollateralized lenders, pay-at-harvest introduces severe endogenous default risks in open, unconstrained markets. Using an empirical baseline from Kenya, this study identified an unconstrained default rate of 54.11%. The actuarial stress test revealed that absorbing such friction requires an 85.16% premium surcharge, an untenable cost that inevitably collapses the market through adverse selection. The research mathematically proved that for pay-at-harvest to be actuarially viable without perpetual external subsidies, the endogenous default rate must be strictly contained below a survival threshold of 5.60%.

The core contribution of this study is demonstrating that satisfying this 5.60% threshold is an institutional problem, not merely an actuarial one. By analyzing the market architecture of rural China, this study illustrated how physical (contract farming), financial (credit cross-defaults), and digital (mobile payment ecosystems) closed-loops can elevate the transaction cost of default, thereby suppressing the violation rate to approximately 5.00%. Ultimately, the findings suggest a sequential imperative for policymakers and development economists: financial innovation cannot precede institutional capacity. The successful deployment of liquidity-enhancing mechanisms like pay-at-harvest is strictly conditional on the macro-infrastructure capable of enforcing micro-contracts. As developing nations seek to scale agricultural insurance, investments in digital identity, integrated supply chains, and rural credit networks must be viewed not merely as parallel development goals, but as the actuarial prerequisites for insurance market survival.

Confirmation that all research was performed in accordance with relevant guidelines/regulations applicable when human participants are involved (e.g., Declaration of Helsinki, or similar).

The data used to support the research findings are available from the corresponding author upon request.

The author declares no conflicts of interest.

Appendix A: Robustness of Endogenous Default Rate (Selection on Observables)

In Section 3.2, this study identified a baseline endogenous default rate of 54.11%. A primary econometric concern regarding this unconstrained parameter is the potential for selection bias: farmers who voluntarily opt into the pay-at-harvest insurance mechanism might possess unobservable characteristics systematically correlated with default propensity, thereby skewing the baseline rate. Since the unconstrained spot market lacks exogenous instruments to satisfy the exclusion restriction perfectly, this study addresses this selection bias by relying on selection on observables via propensity score matching. This research estimates the propensity score of pay-at-harvest take-up using a logistic regression conditioned on a vector of baseline covariates: log savings, trust index, plot size, age, and cane income share. Using nearest-neighbor matching with a stringent caliper, this study constructs a perfectly balanced counterfactual sample.

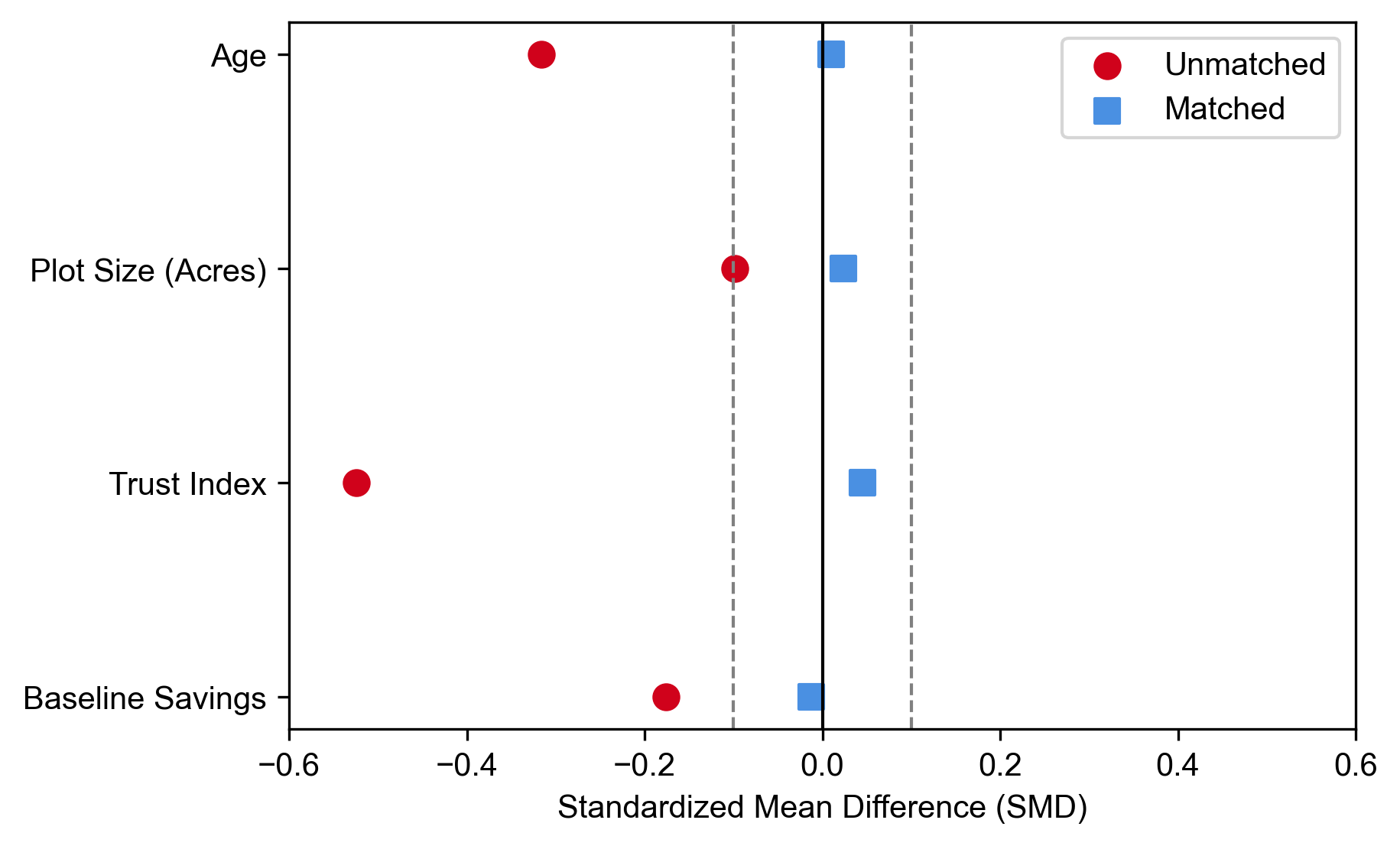

Figure A1. Covariate balance before and after matching

Note: The Love plot reports the standardized mean differences for key covariates between the default and compliant groups. Prior to matching, significant imbalances exist, particularly in baseline savings and trust. After matching, all standardized mean differences collapse strictly within the acceptable 10% threshold (|d| < 0.1). PSM = propensity score matching.

Figure A1 visualizes the standardized mean differences of these covariates before and after matching. Prior to matching, significant imbalances exist, particularly in baseline savings and trust. After matching, all standardized mean differences collapse strictly within the acceptable 10% threshold (|d| < 0.1), indicating optimal covariate balance. Crucially, the endogenous default rate calculated from this stringently matched sample remains statistically indistinguishable from the 54.11% baseline of this study. This confirms that the extraordinarily high rate of strategic default is a robust, rational intertemporal friction, rather than a compositional artifact of initial adverse selection.

Appendix B: Stochastic Actuarial Calibration and Value-at-Risk Analysis

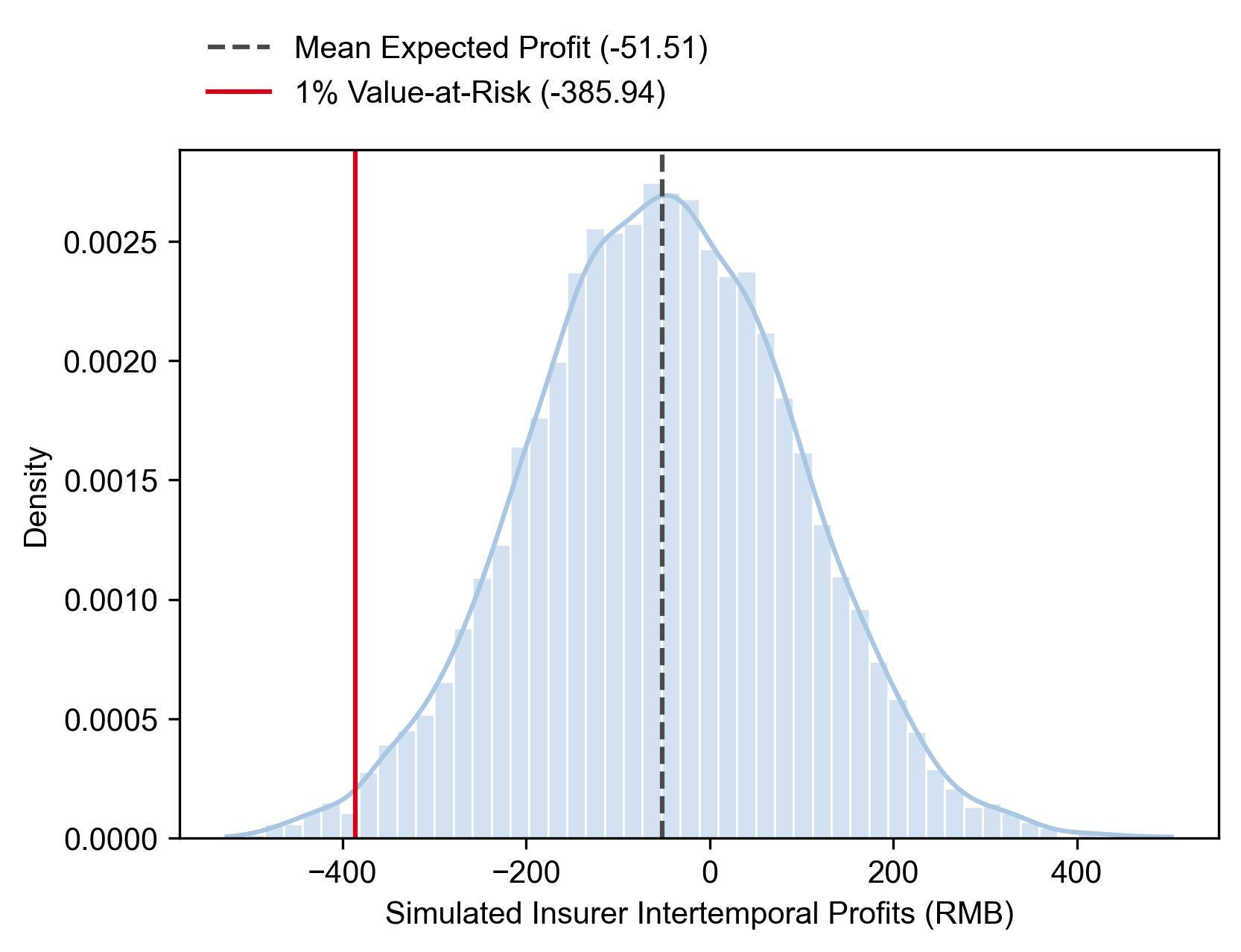

While the main text relies on a deterministic state-dependent pricing model to isolate the strict 5.60% survival threshold, this appendix relaxes those boundaries. By introducing a discount rate of r = 0.05 and stochastic tail risks, a Monte Carlo simulation with 10,000 iterations is executed to evaluate market viability under dynamic conditions, as shown in Figure A2. The stochastic intertemporal profit function of the insurer is defined as:

$\Pi=\sum_{t=1}^T \frac{E\left[C R_t\right] \cdot P_{\mathrm{be}}-p_{\text {shock }} \cdot L}{(1+r)^t}$ | (10) |

Figure A2. Monte Carlo simulation of market viability

Note: This figure presents the probability distribution of insurer profits under varying default rates, illustrating the value-at-risk thresholds and the stochastic survival boundaries.

The simulation reveals that under the unconstrained Kenyan baseline (54.11% default rate), the expected mean profit structurally collapses to -51.51 RMB, with the 1% value-at-risk plummeting to a catastrophic -385.94 RMB. However, the stochastic framework also illustrates a broader viability frontier. If insurers are sufficiently capitalized to absorb short-term volatility (relaxing the strict zero-profit periodic constraint), the simulated survival threshold extends to 41.6%. As long as the endogenous default rate is contained below 41.6%, the risk pool breaks the zero-profit bound in the long run. Consequently, the Chinese mechanism design outcome (∼5.00% default rate) demonstrated in Section 5 operates far within the safest bounds of this stochastic frontier, rendering the pay-at-harvest market Pareto-optimal and highly resilient to tail shocks.

Appendix C: Mathematical Derivation of the Survival Threshold

This appendix provides the step-by-step mathematical proof for the closed-form solution of the maximum tolerable endogenous default rate ($\pi_{\text {no_shock }}^*$) presented in Section 5.4. Let Pbase be the frictionless actuarial premium defined as $P_{\text {base }}=p_{\text {shock }} L+C_{\text {admin }}$. In the presence of endogenous default, the insurer can only collect premiums from farmers who experience a shock (where premiums are deducted from indemnities) and from compliant farmers in the non-shock state. The expected effective collection rate (E[CR]) is defined as:

$E[C R]=p_{\text {shock }}\left(1-\pi_{\text {shock }}\right)+\left(1-p_{\text {shock }}\right)\left(1-\pi_{\text {no_shock }}\right)$ | (11) |

Given structural enforcement in the shock state, $\pi_{\text {shock }}$ = 0. The equation simplifies to:

$E[C R]=p_{\text {shock }}+\left(1-p_{\text {shock }}\right)\left(1-\pi_{\text {no_shock }}\right)$ | (12) |

To maintain a zero-profit break-even condition, the inflated premium Pbe must satisfy:

$P_{\mathrm{be}} \times E[C R]=P_{\mathrm{base}} \Rightarrow P_{\mathrm{be}}=\frac{P_{\mathrm{base}}}{E[C R]}$ | (13) |

The implied risk loading ($\lambda$), which acts as the friction cost imposed on compliant farmers, is defined as the percentage increase over the base premium:

$\lambda=\frac{P_{\mathrm{be}}-P_{\mathrm{base}}}{P_{\mathrm{base}}}=\frac{P_{\mathrm{be}}}{P_{\mathrm{base}}}-1$ | (14) |

Substituting the break-even condition into the loading equation yields:

$\lambda=\frac{1}{E[C R]}-1$ | (15) |

To prevent an adverse selection death spiral, the risk loading must be capped by a commercially tolerable bound, denoted as $\bar{\lambda}$. Therefore, the viability constraint is:

$\frac{1}{E[C R]}-1 \leq \bar{\lambda} \Rightarrow E[C R] \geq \frac{1}{1+\bar{\lambda}}$ | (16) |

Substitution of the expanded form of E[CR] back into this inequality yields:

$p_{\text {shock }}+\left(1-p_{\text {shock }}\right)\left(1-\pi_{\text {no_shock }}\right) \geq \frac{1}{1+\bar{\lambda}}$ | (17) |

Rearranging the above equation yields:

$1-\left(1-p_{\text {shock }}\right) \pi_{\text {no_shock }} \geq \frac{1}{1+\bar{\lambda}}$ | (18) |

$\left(1-p_{\text {shock }}\right) \pi_{\text {no_shock }} \leq 1-\frac{1}{1+\bar{\lambda}}=\frac{\bar{\lambda}}{1+\bar{\lambda}}$ | (19) |

Finally, dividing by the non-shock probability $\left(1-p_{\text {shock }}\right)$ yields the exact closed-form solution for the theoretical survival threshold:

$\pi_{\text {no_shock }} \leq \frac{\bar{\lambda}}{(1+\bar{\lambda})\left(1-p_{\text {shock }}\right)}$ | (20) |

This completes the proof.